The Essense Behind Rental Income and Temporary Account

In the financial accounting realm, businesses allocate different types of incomes and expenditures across various accounts to accurately track and depict their economic activity. One of the prevalent income sources for many firms is leasing revenue. However, confusion often arises about whether this rental income is considered a temporary account.

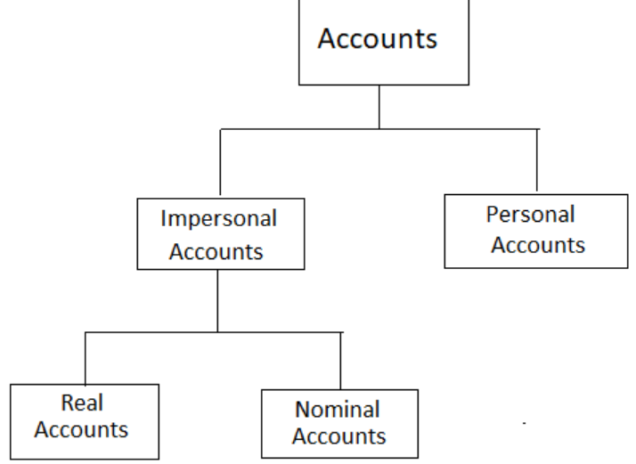

Understanding Temporary Accounts

Before delving into the categorization of rental (or lease) income, it’s crucial to understand what a temporary account signifies. Temporary accounts, also known as nominal accounts, are accounts that record incomes, expenditures, gains, and losses for a specific period, typically a fiscal year. These accounts are labeled “temporary” because they close at the end of the reporting period, transferring their balances to other accounts such as retained earnings or the income summary.

Temporary accounts illustrate financial activities not part of a company’s current operations. They are designed to provide a clear picture of earnings and expenditures over a specific period, aiding in the creation of accurate financial reporting. Examples of temporary accounts include sales revenue, payroll expenses, advertising costs, and interest income.

Examining Rental Income

Rental income is a significant component of revenue for businesses involved in leasing properties or rentals. It is the revenue generated by the business from leasing out real estate properties, such as residential spaces, commercial areas, or office buildings, to lessees in exchange for periodic lease payments.

From an accounting perspective, lease income is classified as revenue and falls under the temporary accounts category. It’s reflected in the income statement, which sums up the company’s revenues, expenses, profits, and losses for a specific period, usually a fiscal year. Temporary accounts, including lease income, close at the end of the reporting period to facilitate the creation of precise financial reporting. This exploration demystifies the temporary nature of rent income in financial accounting and helps address any related confusion.

The recognition of leasing revenue is carried out in accordance with the revenue recognition principle, a fundamental concept of accounting. This principle stipulates:

- Revenue should be recognized at the point of its realization or when it becomes realizable and collectible, regardless of when the payment is received;

- In the case of lease income, it is recognized in the period it is earned, typically based on the terms of the lease agreement.

It’s vital to note that lease payment timelines can differ from income recognition schedules. Lease payments might be received in advance, as a liability, or in parts during the lease term. However, the corresponding lease income is recognized in the reporting period it’s considered earned, regardless of the actual time of payment.

For instance, if a lessee makes a lease payment for the upcoming month in advance, the business reports the lease payment as a liability until the start of the lease period. Following the commencement of the lease period, the leasing revenue is recognized as income in the respective reporting period.

Exceptions to Temporary Classification

Although lease revenue is typically regarded as a temporary account, due to be closed at the end of the reporting period, there are exceptions to this classification. In some situations, lease income can be treated as a permanent account. Here are some scenarios in which lease income might be viewed differently:

Businesses Primarily Engaged in Rental Activities:

If a company’s primary operation involves property leasing, and a significant portion of its earnings comes from leases, then the leasing revenue can be classified as a permanent account.

Such a setup acknowledges the company’s constant income-generating activity when lease income is a substantial and recurring source of revenue.

The lease income is not closed at the end of the reporting period but carried over to the next to accurately depict the continuous operation of the leasing enterprise.

Real Estate Investment Companies:

Real estate investment companies primarily engage in acquiring and leasing out properties with the intent of generating lease income.

Considering the long-term nature of their investments and revenue streams, these companies might categorize leasing income as a permanent account.

The lease income isn’t closed at the end of the reporting period but is carried over to subsequent periods to reflect the company’s ongoing leasing activities.

Improvements to Leased Property:

Improvements to leased property pertain to modifications or enhancements made by the lessee to the leased asset. In certain instances, the costs incurred for the enhancement of the leased property can be depreciated over the lease term. The associated depreciation expenses are then matched with the earnings generated from the lease during the lease term and are treated as permanent accounts.

This approach ensures proper alignment between expenses and corresponding earnings, reflecting the long-term nature of the lease agreement.

Leasehold Improvements:

The income recognition system from a lease can also be influenced by the accounting system the company adheres to, such as GAAP or IFRS:

- These systems may have specific guidelines or requirements that impact the classification of lease earnings;

- To determine the method of lease income accounting in each case, one must familiarize oneself with the specific standards and rules of the applicable accounting system.

It should be noted that the classification of lease income as temporary or permanent is a matter of professional judgment and may vary depending on the circumstances of each business and specific accounting standards. Understanding the unique features of the business and accounting recommendations provided by the respective accounting systems are crucial in determining the appropriate lease income regime.

Generally, lease income is considered a temporary account, due to be closed at the end of the reporting period, yet exceptions exist based on the nature of the business. For instance, if the company primarily engages in leasing activities, real estate investments, or leasehold improvements. Moreover, accounting systems can influence the accounting procedure. These exceptions recognize the permanent and long-term aspects of income generation for some leasing enterprises, ensuring financial reporting accuracy.

FAQ

Yes, lease income is typically considered a temporary account in accounting. As an income account, it falls under the category of temporary accounts, also known as nominal accounts. Temporary accounts track revenues, expenses, gains, and losses for a specific period, typically a fiscal year.

A temporary account, also recognized as a nominal account, represents a category of accounts in financial accounting. It keeps track of revenues, expenditures, gains, and losses for a specific timeframe, typically a fiscal year. The ‘temporary’ nature of these accounts comes from the practice of zeroing their balances at the close of a reporting period, making it easier to gauge net income or loss for that duration.

Accounts that are not considered temporary are known as permanent accounts or real accounts. Contrary to temporary accounts that track revenues, expenses, gains, and losses for a given period, permanent accounts carry their balances over from one reporting period to the next. These accounts provide a cumulative record of the company’s financial position over time.

Lease expense, which refers to payments made under a lease agreement, is not considered a permanent account. Instead, it falls under the umbrella of temporary or nominal accounts. This is because lease expenses, like other costs, are recognized and accrued over specific accounting periods, usually a fiscal year. At the end of each period, the balance is reset to zero in preparation for the next period’s expenses, in line with the principle of matching expenses with the revenues they helped generate within the same period.